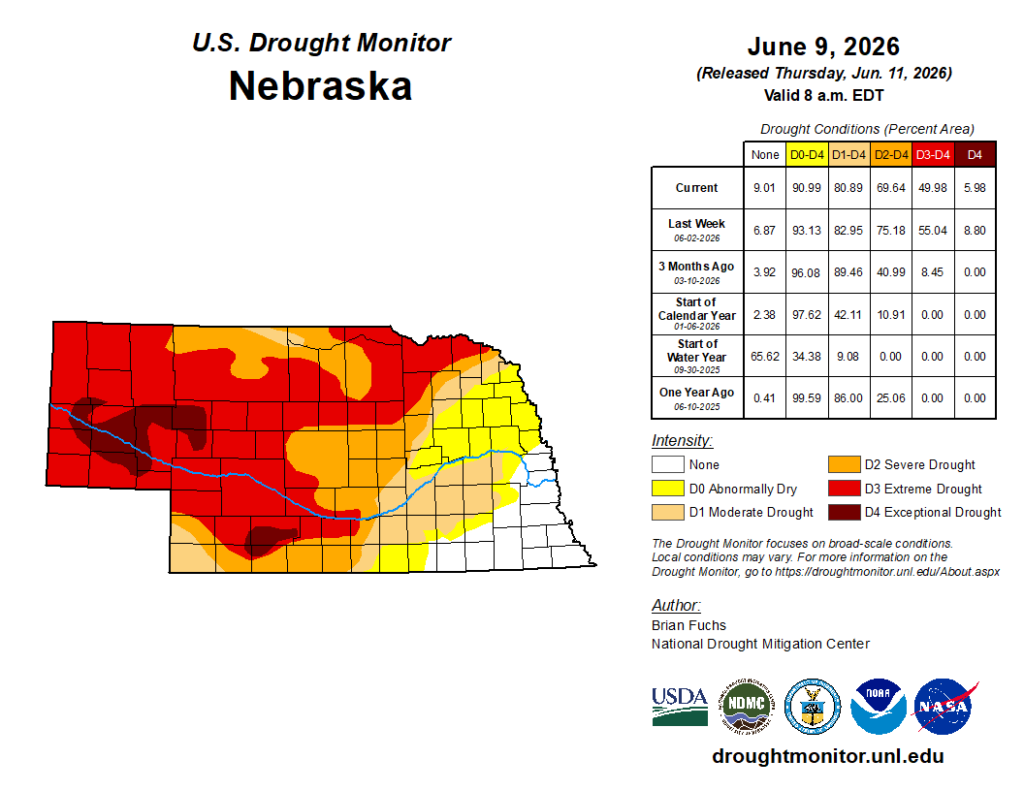

The Drought Monitor released last week shows that much of the western half of the state is still in severe drought (D2) or worse with an area of exceptional drought (D4) in the Panhandle and portions of southwest Nebraska. However, the percentage of all drought categories has improved somewhat in the last few weeks. Furthermore, roughly 20 percent of the state is now free of drought and 9 percent of the state (all southeast NE) has no drought or abnormal dryness.

Recent moisture

The last 30 days have delivered significant moisture to much of south central and southeastern Nebraska, pockets of good moisture to west central sections of the state, and below average precipitation to much of the Panhandle and the area north of O’Neill.

Water-year deficits and surpluses

The water year to date (starting October 1) departure from normal map shows that the rainfall over the past month has led to an eradication of WYTD deficits across much of the southeast quadrant of the state, with some significant surpluses between Beatrice and Auburn. Deficits have improved a bit across southwestern Nebraska. However, deficits are still significant in most of the Panhandle, Sand Hills, and are closing in on 10 inches to the north of O’Neill where exceptional drought was in place the week before.

Soil moisture

The recent precipitation has not necessarily left a truly full profile of root zone moisture (outside a few spots in southeast NE) but it has improved for many of us. Most of south central and eastern Nebraska are now safely above the 30 percent available water threshold in the top 2 meters according to NASA’s SPORTLIS (Short-term Prediction Research and Transition). However, the western half of the state is still short of that mark, meaning vegetation is much more likely to experience stress without supplemental water through irrigation. Fire danger risk will remain elevated on any days with lower humidity and wind until this situation improves.

Weather and Economic

Changes Brings Mixed Blessings

Pat Baxa, Seed Sales Specialist for Polansky Seed out of Belleville, Kansas, has some observations about the current climate.

Baxa told Farming Tool, “Wheat yields will be less than last year mostly due to spring drought stress and late spring freezes. Corn and soybeans have had positive starts due to favorable moisture received except where areas of severe weather from hail and high winds have damaged/destroyed.”

While recent storms have wreaked havoc across central and eastern Nebraska, the rains were definitely needed in that part of the country, that has suffered under drought conditions for years. Baxa put it bluntly, “Precipitation helps everything.”

Of course, it is not just weather that can help or hurt both the farmer and the seed supplier. Increasing expenses for everything from farm equipment to fertilizer to fuel have been putting the squeeze on every element of the ag business for years.

“Rises in fuel cost as any input increase, definitely makes a difference in the bottom line,” said Baxa

.

Recent announcements from the White House about the potential reopening of the Straight of Hormuz, a vital waterway where both oil and urea (an important component of fertilizer) bring hopes that both fertilizer and fuel costs may soon come. However, it is unclear how soon the ag business will see those reductions or if they will, in turn, translate into cost reductions in all the other things farmers and their suppliers must buy to keep operating.

Lindberg Family Farms has been irrigating crops for several decades as the farm was purchased 80 years ago. Like many operations in the region, irrigation began with siphon tubes and eventually evolved into graded irrigation pipe systems. While effective for their time, those methods typically deliver only about 50–60% irrigation efficiency. As water supplies have tightened over the years, Lindberg realized a more efficient solution was needed.

The farm moved to center pivot irrigation, installing one pivots in 2009. But the most significant change came recently. In 2024, Richard installed another and retrofitted the original system with variable rate irrigation (VRI) capabilities.

In 2025, Roehr’s Machinery in Beatrice, Neb., helped Lindberg by installing two new Reinke Electrogator II pivots. They also added Reinke’s award winning electronic swing arm corner (ESAC) technology to walk the pivot past their barn, adding valuable acres under pivot. The Reinke dealer installed RPM Touch Screen control panels and the RC10 monitoring system, helping Lindberg with remote management to save valuable resources while still putting down the water his crops needed.

“The dealer helped us plan the whole thing,” Lindberg said. “We put up the new Electrogator pivots and got soil sensors out in the fields. Now I can control the whole thing with my phone instead of driving around to check and make sure the pivots were getting water to the crops.”

Water savings a “major turnaround”

The time savings was a big bonus, but the best part came later in the season when he could see how much less water they’d used.

“For the first time ever, we didn’t run out of water during the growing season,” he said. “Historically, we’d always had to shut off the water well before we wanted. This was a major turnaround for us.”

That milestone marked a major turnaround for the farm. In previous years, water allocations often ran dry before crops finished their growth cycle. With the new pivots and precision controls, the farm managed its entire season without exhausting its water supply.

Lindberg credits Reinke’s irrigation equipment and technology along with the support from the Republic County Conservation District, grant funding and assistance from the local Farm Service Agency to help make the upgrades possible.

“We couldn’t have made these improvements ourselves,” he said. “This has all really been a blessing for us.”

Reinke irrigation solutions make all the difference

The technology allowing Lindberg to irrigate fields with precision water application is integrated to work with CropX sensor to monitor soil moisture, crop behavior and soil health. The sensor collects the data and feeds back watering recommendations to the Electrogator II pivot.

“Richard can easily access the information he needs on his smart phone without having to drive out to the field and check the pivots manually,” said Eric Bathel at Roehr’s Machinery. “The field layout was challenging, but with the addition of a swing arm we were able to get nearly 90% coverage of his total acres and made a dramatic difference in their irrigation water usage. From one year to the next, they could certainly see the difference in how much they saved.”

For Lindberg, investing in modern irrigation isn’t just about efficiency – it’s about conserving resources and protecting the future of farming that his family has done for generations.

For more information on grants to help purchase precision irrigation equipment, find your state’s Natural Resources Conservation Service office by visiting NRCS.USDA.gov. To find out more about Reinke’s complete line of irrigation solutions or to find a dealer near you, go to Reinke.com.

by Olivia L’Ecuyer/Farming Tool Magazine

‘Beef, it’s what’s for dinner,’ is a common saying that many rural living individuals might say or hear a few times a year. This saying is becoming more and more true as the markets for beef cattle continue to rise and make a solid profit for many farmers and ranchers. As the beef cattle market continues to rise, there are more and more concerns from many farmers and ranchers on how the cattle market will be for the rest of 2025 and continuing into 2026.

The first six months of 2025 have been marked by higher cattle and beef prices which has been driven by high cattle inventories and supply restraints. In Nebraska, feeder steer prices continue to set record highs and in April prices hit nearly $400/cwt which was nearly $150/cwt higher than that same time last year. In Kansas, fed cattle traded at US$237, steady to $2 higher, while Nebraska saw dressed trade up to $5 stronger. Wholesale beef values also surged, with the choice cutout climbing nearly $15 to $393.80. Packers are running on negative margins, trimming kills and tightening supply, while demand remains absolutely amazing.

So what is driving the prices to go up in the cattle market? That would be due to the U.S. cattle numbers that have declined over the past few years. In 2024, Nebraska’s calf crop was down 18 percent from 2018, which was the most recent high and the smallest in at least 35 years. In 2025, Kansas ranked third nationally with 5.95 million cattle on ranches and feedyards as of January 1, 2025 and in 2023 cattle and calves represented 58 percent of Kansas’s agricultural cash receipts. The prices over the first seven months of 2025 have increased tremendously compared to a year ago for all classes of cattle. Because prices have continued to increase for all sectors, profits will generally be seen by cow-calf producers, stocker-yearling operators and cattle feeders. In previous years, they have begun moving towards increasing calf supplies through retaining heifers for breeding. With the current, widespread rain,, it seems likely that cow herd building through the retaining of heifers will soon be underway; if it is not already.

An article by Aaron Berger, a Nebraska Extension agent and livestock educator shares some of his knowledge about price risk management and how farmers and ranchers are reacting to this change.

“When prices are at profitable levels, have been going up and are going higher, there is usually the temptation to do nothing from a price risk management standpoint,” Berger said. “Frequently folks who spend money on price protection or forward contracted cattle, just to see the price go roaring higher, find themselves questioning if using price protection is prudent when they are feeling the recent disappointment of having left ‘money on the table.’”

This is usually where taking the time to pause and look back at what has occurred with high prices in the past can bring perspective. In previous times, periods of exceptional profitability, those seasons have been followed by times of significant price decline. How soon and how far prices will fall is unknown. However, cattle are still a commodity, and the prices paid for a commodity, over time historically, have generally moved towards breakeven.

So how will the cattle market look for the rest of 2025 and going into 2026? Based on a report from the USDA economic research website, the mid-year Cattle report, a further tightening is expected of calves available for placement in late 2025 and early 2026. The report also suggests steady but gradual changes to inventories of beef cows and replacement heifers. Due to this, 2025 and 2026 beef production forecasts are reduced from last month. Cattle prices are estimated to rise significantly in both the second half of 2025 and in 2026 on recent cattle price reports, strong beef prices, and tighter cattle supplies. Beef imports for 2025 and 2026 have also been revised considerably downward as limited imports from Brazil are expected.

The beef export forecast for 2025 is raised on recent trade data and continued strong demand from key export markets. The beef import forecast is also raised on strong imports from Oceania and South America, as well as robust domestic demand for lean processing beef. Cattle price forecasts for 2025 are raised on recent price strength and continued demand for cattle. The increased price forecasts are carried over into 2026 as well.

Stephen Koontz, researcher at Colorado State University, reports his estimates for cattle in late 2025 and going into 2026.

“For 500- to 600-lb. calves, first-quarter projections are $310 to $315/cwt., second quarter $325 to $340, third quarter $310 to $315 and fourth quarter $300 to $310. First-quarter calf price to average $300/cwt. For the second quarter, the forecast is a $305 average price, third quarter $300 and fourth quarter $300,” Koontz said. “If we were to start to see rapid herd rebuilding, then prices would increase even more due to the lack of heifers on the market. Fewer calves for sale boosts prices for 2025. It’s likely that we need higher prices to get ranchers to increase herds. First-quarter projections for 700- to 800-lb. prices average $250/cwt. For the second quarter, the estimates are $260 average price, third quarter $270 and fourth quarter $270.”

Koontz forecasts first-quarter, fed cattle prices to range between $187.50 and $190/cwt, second-quarter prices from $190 to $200, with third quarter from $190 to $195, and fourth quarter at $195 to $200.

“Again, tight supplies will remain. We will make up for lost numbers with much heavier weights,” he says. “I also think we’ll continue to see corn prices pressured – and this leads to heavier weights and more future pressure on the topside.” Koontz also sees strong cull cow prices, as consumers spend more of their beef dollars on ground beef. Prices will vary, depending on the number of cattle imported for hamburger. Forecasts for the first-quarter, cull cow prices at $85 to $115/cwt., with the second-quarter prices from $115 to $130. His third-quarter projections are from $110 to $130 and fourth quarter at $100 to $120.

With the cattle markets increasing and being predicted to stay at a somewhat steady pace, it looks like farmers and ranchers will be able to earn a solid profit for the rest of 2025 and into 2026.